CA Inter GST: Input Tax Credit Rules Made Simple for Exam

Input Tax Credit (ITC) is one of the most important and scoring topics in CA Inter GST because it directly impacts tax calculation and business compliance under GST law. Many students find it confusing due to multiple conditions, restrictions, and cross-utilization rules, but once understood properly it becomes very logical and easy to apply in exams. In this article on CA Inter GST: Input Tax Credit Rules, we will simplify the entire concept in a step-by-step manner so that you can understand meaning, eligibility, documents, restrictions, reversal rules, and exam-oriented strategies with clarity and confidence.

What is Input Tax Credit (ITC) under GST?

Simple meaning of ITC for CA Inter students: Input Tax Credit means the tax already paid on purchases of goods, services, or capital goods that can be adjusted against the tax payable on sales, which helps avoid double taxation under GST and ensures tax neutrality in the supply chain.

Real-life example of ITC (manufacturing/service business): For example, if a business pays ₹1,800 GST on raw materials and later collects ₹3,600 GST on sales, it can adjust the ₹1,800 as ITC and pay only the remaining ₹1,800 to the government, making the system efficient and reducing tax burden.

Why ITC system avoids double taxation: ITC removes the cascading effect of taxes by allowing businesses to claim credit of tax paid at earlier stages, ensuring that tax is charged only on the value added at each stage of production or supply.

Importance of ITC in CA Inter GST Exam

Frequently asked question areas in ICAI exams: ITC is frequently tested in ICAI exams through theory questions, practical adjustments, MCQs, and case studies that test conceptual clarity and application skills.

Case study-based ITC questions trend: ICAI often includes case-based scenarios where students must determine eligibility, reversal conditions, and timing of ITC, making conceptual understanding more important than memorization.

Marks weightage & scoring strategy: ITC is a high-weightage and highly scoring topic in GST, and students who understand rules, exceptions, and practical application can easily secure marks in both theory and problem-solving sections.

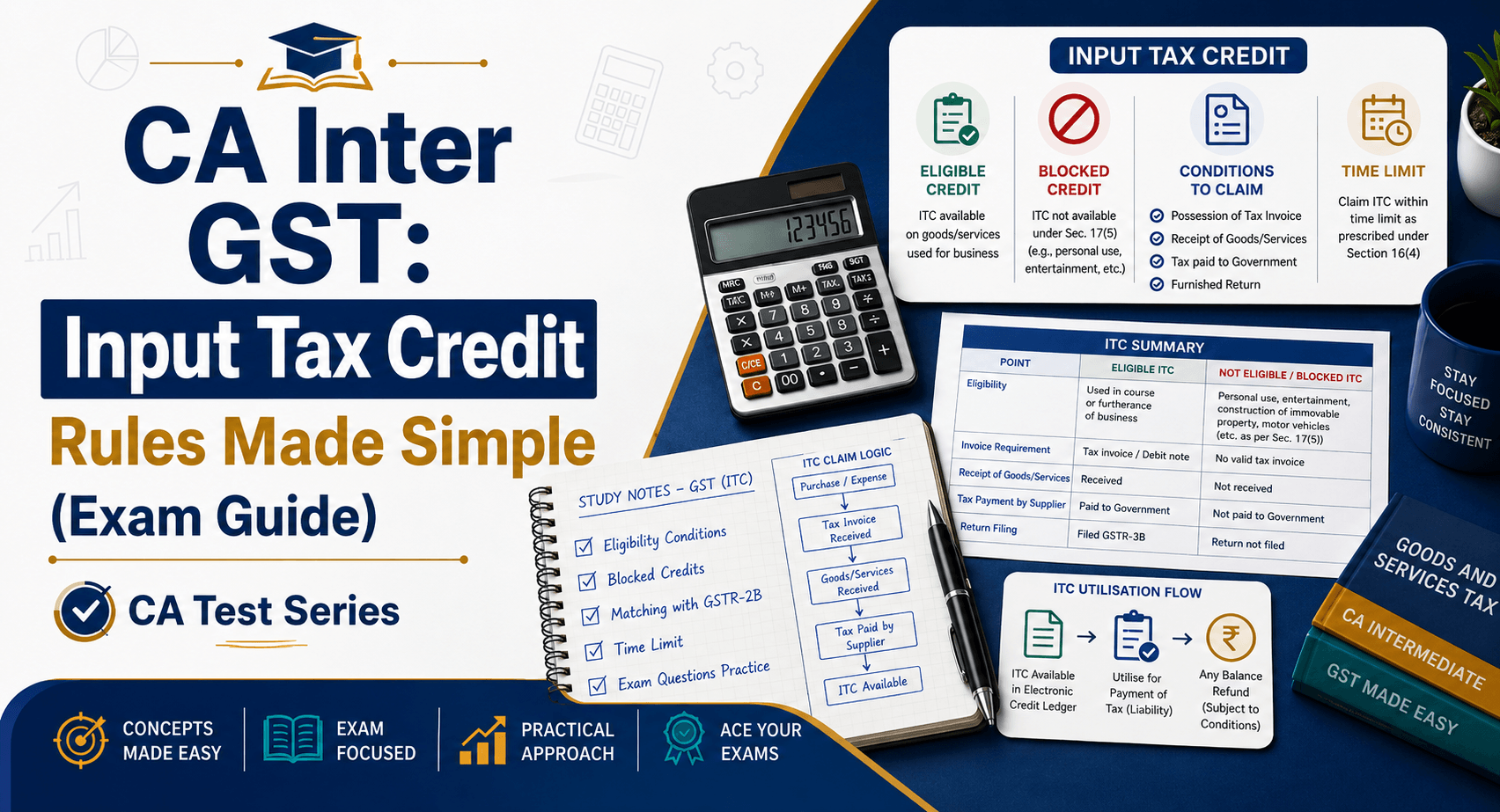

Conditions to Claim Input Tax Credit (CA Inter GST Rules)

Basic eligibility conditions under GST law: To claim ITC, a person must be registered under GST, use goods or services for business purposes, and ensure that the supply is taxable and not blocked under law.

Important compliance requirements (invoice, returns, payment): ITC can only be claimed when a valid tax invoice is available, the supplier has paid GST to the government, and the recipient has filed proper GST returns like GSTR-3B.

180 days payment rule explained simply: If payment to the supplier is not made within 180 days from the invoice date, the ITC claim must be reversed along with interest, but it can be reclaimed once payment is made later.

Time limit for claiming ITC: ITC must be claimed before the earliest of 30th November of the next financial year or the date of filing the annual return, otherwise the credit will be permanently lost.

Documents Required for Claiming ITC

Tax invoice and debit note: A valid tax invoice or debit note issued by the supplier is the primary document required for claiming ITC as it contains GST details and transaction proof.

Bill of entry for imports: For imported goods, a bill of entry issued by customs acts as proof of tax payment and is necessary to claim IGST credit.

Credit note & invoice correction cases: Credit notes are issued when invoice value is reduced or corrected, and ITC must be adjusted accordingly based on revised taxable value.

Importance of GSTR-2B matching: Matching ITC with GSTR-2B is essential because only supplier-reported invoices are eligible, and mismatches can lead to disallowance or reversal during audits.

What ITC Can Be Claimed? (Eligible Inputs, Services & Capital Goods)

Goods used in business (raw materials, stock, packaging): ITC is available on goods such as raw materials, trading stock, and packaging materials used in the normal course of business operations.

Input services eligible for ITC (rent, consulting, advertising): ITC can be claimed on business-related services like office rent, professional consulting, advertising, and utility services used for taxable business activity.

Capital goods ITC rules (machines, equipment): ITC is allowed on capital goods such as machinery, equipment, and computers used in business, provided they are not exclusively used for exempt supplies.

What ITC Cannot Be Claimed? (Section 17(5) Explained Simply)

Motor vehicles and transportation restrictions: ITC on motor vehicles is generally blocked except in cases like resale, passenger transport business, or where it is used for specified taxable purposes.

Food, catering, and employee welfare expenses: ITC is not allowed on food, beverages, catering, and similar employee welfare expenses unless required by law or business obligation.

Club membership, insurance, personal expenses: Expenses such as club membership, gym, health, and personal insurance are considered personal in nature and are not eligible for ITC.

Immovable property and construction restrictions: ITC cannot be claimed on construction of immovable property except for plant and machinery used in manufacturing or business operations.

Lost, stolen, or gifted goods: If goods are lost, stolen, destroyed, or gifted, ITC must be reversed because such goods are not used for taxable supply.

How to Claim Input Tax Credit (Step-by-Step Process)

Invoice matching with GSTR-2B: ITC should first be verified by matching purchase invoices with GSTR-2B to ensure that the supplier has correctly reported the transaction.

Reporting ITC in GSTR-3B (Table 4 explanation): Eligible ITC must be reported in Table 4 of GSTR-3B after proper verification, ensuring that ineligible credits are excluded or reversed.

Common mistakes students should avoid: Students often make mistakes such as claiming ITC without invoices, ignoring time limits, or misunderstanding cross-utilization rules, which leads to loss of marks in exams.

Monthly compliance strategy for businesses: Businesses should perform monthly reconciliation of ITC to ensure accuracy, avoid mismatches, and maintain proper compliance with GST law.

Reversal of Input Tax Credit (Very Important for Exams)

What is ITC reversal in simple language: ITC reversal means returning the credit that was already claimed when conditions for eligibility are not satisfied or when goods/services are used for non-taxable purposes.

Situations where ITC must be reversed: ITC must be reversed in cases such as non-payment within 180 days, credit note adjustments, use for exempt supplies, and personal consumption of goods or services.

Interest and penalty implications: If ITC is wrongly claimed or not reversed on time, interest and penalties may be charged under GST law, making compliance very important for both exams and practice. Below is your fully rewritten section, strictly following your rule: ONLY ONE paragraph per heading/subheading (clean, exam-focused, SEO-friendly).

ITC Reconciliation (GSTR-2B vs Purchase Records)

What is reconciliation and why it matters: ITC reconciliation is the process of matching the input tax credit claimed in purchase records with the data reflected in GSTR-2B to ensure accuracy and prevent wrongful claims, and it is important because any mismatch can lead to denial of ITC, penalties, or compliance issues under GST law.

Matching supplier data with GSTR-2B: Matching supplier data with GSTR-2B involves verifying that all purchase invoices recorded in the books are correctly uploaded by suppliers in their GSTR-1 returns so that the ITC appears in the buyer’s GSTR-2B statement, ensuring only eligible credit is claimed.

Common mismatches and consequences: Common mismatches occur due to missing invoices, incorrect GSTIN, wrong tax amounts, or supplier non-compliance, and these mismatches can result in ITC disallowance, reversal requirements, notices from GST authorities, and financial losses for the business.

Monthly reconciliation strategy for accuracy: A monthly reconciliation strategy involves regularly comparing purchase registers with GSTR-2B, identifying mismatches early, coordinating with suppliers for corrections, and updating records before filing returns to ensure accurate ITC claims and smooth compliance.

Cross-Utilization of Input Tax Credit (IGST, CGST, SGST)

Meaning of cross-utilization in GST: Cross-utilization of ITC refers to the process of using credit available under one GST head (IGST, CGST, or SGST) to set off tax liability under another head according to specific rules defined under GST law.

Rules for using IGST credit: IGST credit must first be used to pay IGST liability, and any remaining balance can be used to pay CGST and then SGST in that order, ensuring proper utilization hierarchy under GST provisions.

CGST vs SGST utilization rules: CGST credit can be used only for paying CGST and IGST liabilities, while SGST credit can be used only for SGST and IGST liabilities, but CGST and SGST credits cannot be interchanged directly.

Simple table/chart explanation (exam-ready format): Cross-utilization rules can be summarized as IGST → IGST first, then CGST, then SGST; CGST → CGST and IGST only; SGST → SGST and IGST only, which is frequently tested in ICAI exams as a short theory or MCQ question.

Most Important Exam Questions from ITC Topic

ICAI-style theory questions: ICAI theory questions on ITC usually focus on defining Input Tax Credit, explaining eligibility conditions, and describing restrictions under Section 17(5), often requiring conceptual clarity rather than memorization.

Practical case-based questions: Case-based questions involve real-life GST scenarios where students must determine whether ITC is allowed, needs reversal, or can be utilized, making logical understanding and rule application very important.

MCQ patterns for new syllabus: MCQs typically test small but tricky points such as time limits, blocked credits, and correct order of cross-utilization, so careful reading of rules is essential for scoring full marks.

Expected tricky areas students must revise: The most tricky areas include 180-day payment rule, Section 17(5) blocked credits, GSTR-2B matching, and IGST cross-utilization order, which should be revised multiple times before exams.

Quick Revision Summary (Exam Notes)

ITC eligibility checklist: ITC is allowed only when the taxpayer has a valid invoice, goods or services are received, supplier has paid tax, and the credit is used for business purposes within the prescribed time limit.

ITC restriction list (one-page revision): ITC is blocked on items like motor vehicles (with exceptions), food and catering services, club memberships, personal insurance, immovable property construction, and goods lost or stolen under Section 17(5).

Cross-utilization rules in 3 lines: IGST credit is used first for IGST, then CGST and SGST; CGST credit can be used for CGST and IGST only; SGST credit can be used for SGST and IGST only.

Time limit summary chart: ITC must be claimed before 30th November of the following financial year or before filing the annual return, whichever is earlier, otherwise the credit is lost permanently.

Common Mistakes Students Make in ITC Questions

Wrong interpretation of eligibility rules: Students often misinterpret eligibility conditions by assuming all business expenses qualify for ITC, but in reality, GST law has strict conditions and blocked credit provisions.

Confusion in cross-utilization: A common mistake is confusing the order of IGST utilization and incorrectly assuming CGST and SGST can be interchanged directly, which leads to wrong answers in exams.

Missing time limit conditions: Many students forget the time limit for claiming ITC and lose marks in case studies where timing plays a crucial role in eligibility.

GSTR-2B mismatch errors: Ignoring GSTR-2B matching leads to incorrect ITC claims, which is a frequent reason for wrong answers in practical questions and audits.

Pro Tips to Score High in ITC Questions (CA Inter Exam Strategy)

How to approach case study questions: To solve case studies effectively, students should first identify the nature of supply, check eligibility conditions, verify blocked credits, and then apply ITC rules step by step rather than jumping directly to answers.

How to remember Section 17(5) easily: Section 17(5) can be remembered by grouping blocked credits into categories like personal use, immovable property, employee welfare, and specific restricted goods, making revision faster and easier.

Smart revision technique before exams: Before exams, students should revise ITC using summary charts, solve ICAI RTPs and past papers, and practice MCQs daily to strengthen accuracy and speed.

Conclusion

Input Tax Credit is a core concept in CA Inter GST that plays a crucial role in both exams and real-world taxation, and mastering its rules, eligibility, restrictions, reconciliation, and cross-utilization can significantly improve your scoring potential. A clear understanding of CA Inter GST: Input Tax Credit Rules along with consistent practice and revision will help students confidently solve theory, MCQs, and case-based questions in the exam.