CA Inter Income Tax: Deductions Under Chapter VI-A Covered Completely

Chapter VI-A deductions are an important part of CA Inter Income Tax because they directly affect the computation of taxable income. These deductions allow eligible taxpayers to reduce their Gross Total Income by claiming specific investments, expenses, donations, loan interest, medical insurance payments, and other qualifying amounts under the Income-tax Act. For CA Inter students, this topic is highly important because it is commonly tested in both theory and practical questions. A small mistake in applying deduction limits, eligible assessee rules, or payment mode conditions can change the final taxable income. That is why students must understand not only the section names but also how each deduction is applied in exam-style questions.

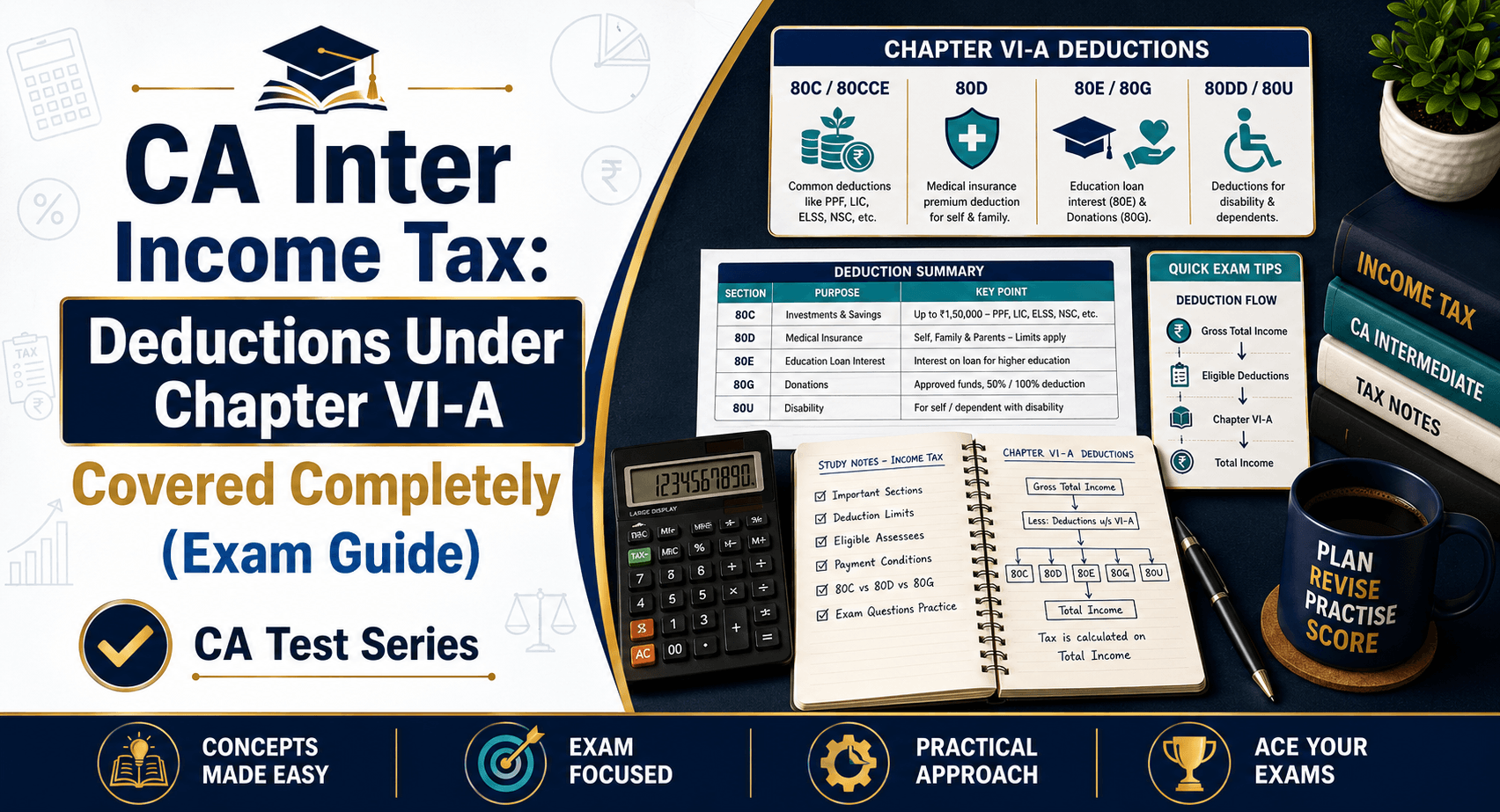

What Are Chapter VI-A Deductions?

Chapter VI-A deductions are deductions allowed from Gross Total Income to calculate Total Income. These deductions are covered under sections such as 80C, 80D, 80E, 80G, 80TTA, 80TTB, and other related provisions. In simple terms, first income is calculated under different heads such as salary, house property, business income, capital gains, and other sources. After that, eligible deductions under Chapter VI-A are reduced from Gross Total Income. The balance amount is known as Total Income, on which tax is calculated.

Basic Concept of CA Inter Income Tax Deductions

Before studying the individual sections, CA Test Series students should clearly understand the difference between Gross Total Income and Total Income. Gross Total Income means the total income computed before claiming deductions under Chapter VI-A. Total Income means Gross Total Income minus eligible Chapter VI-A deductions. This distinction is important because deductions are not deducted directly from each income head. They are claimed only after Gross Total Income is calculated. Another important concept is the difference between exemption and deduction. An exemption is excluded from income itself, while a deduction is reduced after income is computed. For example, exempt income may not form part of total income, but deductions under Chapter VI-A are claimed from Gross Total Income.

Important Chapter VI-A Deductions for CA Inter

The following deductions are most relevant for CA Inter Income Tax preparation. Students should revise these sections carefully because they are frequently used in practical computation questions.

1. Section 80C: Investment-Based Deduction: Section 80C is one of the most important deductions under Chapter VI-A. It is available to individuals and HUFs for specified investments and payments such as life insurance premium, Public Provident Fund, tuition fees, repayment of housing loan principal, tax-saving fixed deposits, and other eligible items. This section is important in CA Inter exams because questions often include both eligible and ineligible payments. Students must identify which payments qualify and apply the correct limit.

2. Section 80CCC and Section 80CCD: Pension and NPS Deduction: Section 80CCC allows deduction for contribution to specified pension funds. Section 80CCD deals with contributions to the National Pension System. It includes employee contribution, additional NPS contribution, and employer contribution. Students should remember that Section 80C, Section 80CCC, and Section 80CCD(1) are subject to the overall limit under Section 80CCE. However, additional NPS deduction and employer contribution may have separate treatment depending on the relevant sub-section.

3. Section 80D: Medical Insurance Deduction: Section 80D allows deduction for medical insurance premium paid for self, spouse, dependent children, and parents. It also includes preventive health check-up within the prescribed limit. A key exam point is payment mode. Medical insurance premium should not be paid in cash, but preventive health check-ups can be paid in cash. Students should also check whether the insured person is a senior citizen because the deduction limit may differ.

4. Section 80DD, 80DDB and 80U: Disability and Medical Treatment Deductions: These sections are often confusing for students. Section 80DD applies when the assessee incurs expenditure for a dependent person with disability. Section 80DDB applies for medical treatment of specified diseases. Section 80U applies when the assessee himself or herself is a person with disability. The main difference between Section 80DD and Section 80U is the person for whom the deduction is claimed. If the dependent person has a disability, Section 80DD applies. If the assessee has a disability, Section 80U applies.

5. Section 80E: Interest on Education Loan: Section 80E allows deduction for interest paid on an education loan taken for higher education. The loan may be taken for the assessee, spouse, children, or a student for whom the assessee is a legal guardian. Only the interest portion is allowed as a deduction. Principal repayment is not allowed under Section 80E. This section is simple but frequently tested in practical questions.

6. Section 80EE, 80EEA and 80EEB: Loan Interest Deductions: Sections 80EE and 80EEA relate to interest on housing loans, while Section 80EEB relates to interest on loans taken for the purchase of an electric vehicle. These deductions have specific conditions related to loan sanction period, property value, and type of loan. Students should compare these provisions carefully with Section 24(b), because housing loan interest may appear in both house property computation and Chapter VI-A deduction questions.

7. Section 80G: Donation-Based Deduction: Section 80G allows deduction for donations made to specified funds and approved charitable institutions. Some donations qualify for 100% deduction, while others qualify for 50% deduction. Some donations are subject to qualifying limits, while others are not. A common exam mistake is ignoring the cash payment restriction. Students must check the payment mode before allowing deduction under Section 80G.

8. Section 80TTA and Section 80TTB: Interest Income Deduction: Section 80TTA provides deduction for savings account interest to eligible individuals and HUFs. Section 80TTB provides a deduction to resident senior citizens for interest income from specified deposits. Students should not claim both sections for the same assessee. Section 80TTB is specifically for senior citizens and covers a wider range of interest income.

Chapter VI-A Deduction Summary Table

| Section | Nature of Deduction | Eligible Assessee | Important Exam Note |

| 80C | LIC, PPF, tuition fees, housing loan principal | Individual / HUF | Covered under overall limit |

| 80CCC | Contribution to pension fund | Individual | Included in overall limit |

| 80CCD | NPS contribution | Individual | Separate rules for own and employer contribution |

| 80D | Medical insurance premium | Individual / HUF | Premium should not be paid in cash |

| 80DD | Dependent person with disability | Resident Individual / HUF | Fixed deduction based on disability level |

| 80DDB | Specified disease treatment | Resident Individual / HUF | Based on actual expense and age |

| 80E | Interest on education loan | Individual | Only interest is allowed |

| 80G | Donations | Eligible assessee | Check percentage, limit, and payment mode |

| 80TTA | Savings account interest | Individual / HUF | Not for senior citizens claiming 80TTB |

| 80TTB | Interest income for senior citizens | Resident senior citizen | Wider coverage than 80TTA |

How to Solve Chapter VI-A Questions in CA Inter Exams

Students should follow a step-by-step approach while solving Chapter VI-A practical questions. First, compute income under all relevant heads and arrive at Gross Total Income. Second, identify each payment, investment, expense, or donation given in the question. Third, match each item with the correct deduction section. Fourth, check the eligible assessee, deduction limit, and payment mode. Finally, deduct the eligible amount from Gross Total Income to calculate Total Income. This method helps avoid common mistakes such as claiming ineligible payments, applying the wrong limit, or allowing the same deduction twice.

Common Mistakes Students Should Avoid

Many students lose marks in Chapter VI-A questions even after knowing the provisions. The most common mistake is confusing Gross Total Income with Total Income. Deductions are claimed from Gross Total Income, and the balance is Total Income. Another common mistake is applying the wrong deduction limit. Each section has a separate rule, and students should not use one common limit for all deductions. Payment mode conditions are also important, especially in Section 80D and Section 80G. Students also confuse Section 80DD with Section 80U. Section 80DD is for a dependent person with disability, while Section 80U is for the assessee with disability. The overall limit under Section 80CCE should also be remembered while dealing with Section 80C, 80CCC, and 80CCD(1).

Quick Revision Notes for CA Inter Income Tax Deductions

For quick revision, students should prepare a short table containing section number, eligible assessee, nature of deduction, maximum limit, payment mode, and special conditions. This will help in last-minute revision before the exam. Students should especially revise Sections 80C, 80CCD, 80D, 80E, 80G, 80TTA, and 80TTB because these sections are commonly tested in practical questions. For theory and MCQs, students should also revise Sections 80DD, 80DDB, 80U, 80EE, 80EEA, 80EEB, and 80JJAA.

Practice Chapter VI-A with CA Test Series

Only reading the provisions is not enough to score well in CA Inter Income Tax. Students must practice chapter-wise questions and ICAI-pattern mock tests to understand how deductions are applied in practical problems. CA Test Series helps CA Inter students prepare Chapter VI-A through chapter-wise test practice, full syllabus mock exams, expert answer evaluation, and performance feedback. This allows students to identify weak areas, improve presentation, and build confidence before the exam.

Conclusion

CA Inter Income Tax deductions under Chapter VI-A are important for both concept clarity and exam scoring. Students should understand Gross Total Income, apply section-wise deduction rules correctly, remember important limits, and avoid mistakes related to eligibility and payment mode. With regular revision and proper practice, Chapter VI-A can become a scoring area in CA Inter Taxation. Students should solve practical questions, revise deduction limits, and attempt ICAI-pattern tests to improve accuracy and exam performance.