CA Final Group 1 vs Group 2: Risk-Reward Analysis for Both Attempts

Choosing between CA Final Group 1 and Group 2 is one of the most important decisions for CA Final students. The right choice can improve confidence, reduce pressure, and increase the chance of clearing the exam, while the wrong choice can lead to stress, incomplete revision, and poor performance. This detailed guide on CA Final Group 1 vs Group 2 explains the risk, reward, subject difficulty, scoring potential, preparation strategy, and practical decision-making approach for students planning their next CA Final attempt.

CA Final Group 1 vs Group 2: Quick Comparison

CA Final Group 1 and Group 2 are both challenging, but they test different strengths. Group 1 is more focused on financial reporting, finance, audit, and professional judgement, while Group 2 is more focused on taxation, indirect tax laws, amendments, and case-study-based business application. Students should compare both groups based on their subject comfort, available preparation time, revision status, and mock test performance instead of choosing only by popularity or peer pressure.

Comparison Area | CA Final Group 1 | CA Final Group 2 |

| Main Subject Nature | Accounting, finance, audit | Taxation, indirect tax, case studies |

| Preparation Style | Concept clarity and numerical practice | Repeated revision and application |

| Main Risk | Technical complexity and time pressure | Forgetting provisions and amendments |

| Main Reward | Strong technical confidence | Good scoring opportunity with revision |

| Best For | Students strong in practical subjects | Students strong in tax and case studies |

CA Final Group 1 Overview

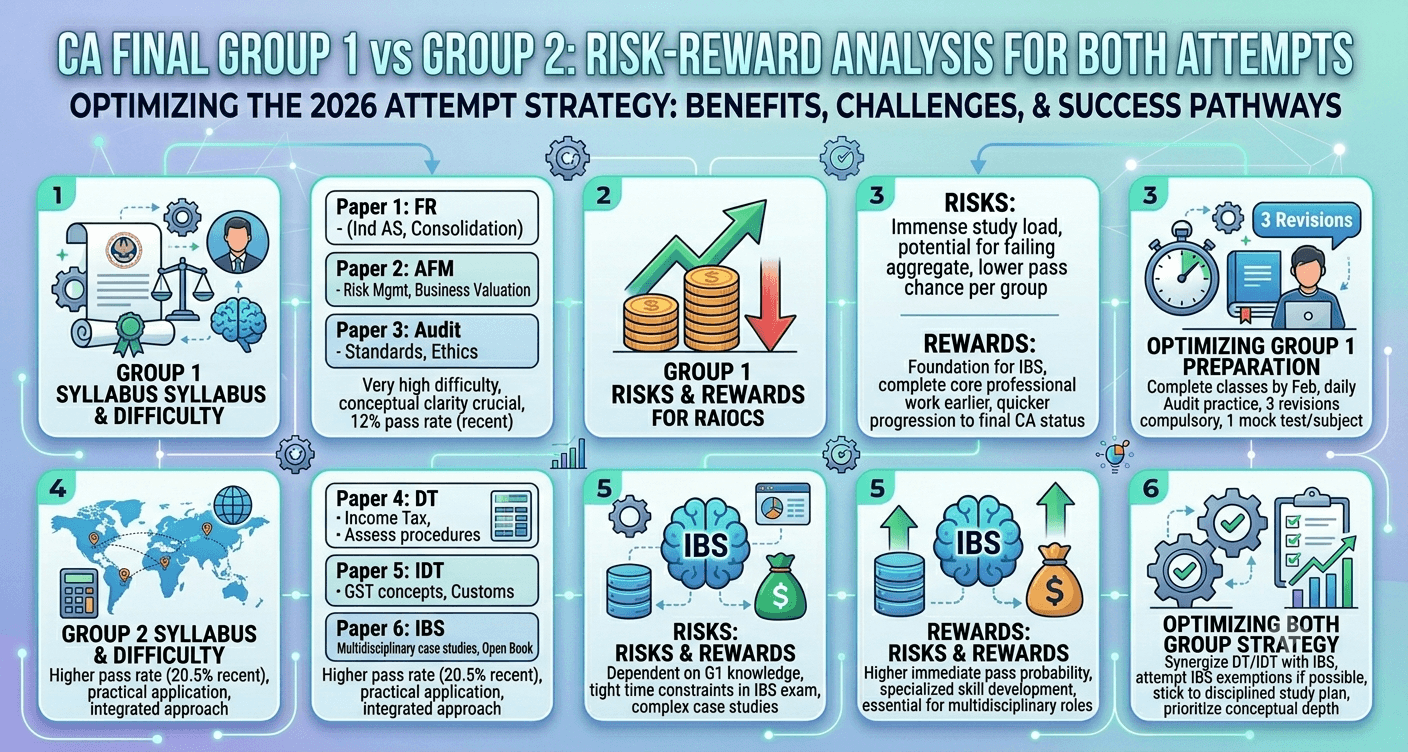

CA Final Group 1 includes Financial Reporting, Advanced Financial Management, and Advanced Auditing, Assurance and Professional Ethics. This group is suitable for students who are comfortable with technical concepts, accounting standards, finance-based calculations, audit procedures, and professional writing. The reward of clearing Group 1 first is that students complete a concept-heavy part of the CA Final syllabus early, but the risk is high if they do not practise enough practical questions or ignore answer presentation in auditing.

Key Risks in Group 1: The biggest risks in Group 1 are weak conceptual clarity, poor numerical practice, lack of time management, and incomplete audit writing preparation. Financial Reporting and Advanced Financial Management can become lengthy in the exam if students have not solved enough full-length questions. Advanced Auditing also needs structured answers, relevant terminology, and professional judgement, so students who only read theory without writing practice may lose marks even if they understand the topic.

Key Rewards in Group 1: The main reward of attempting Group 1 is that it builds strong confidence in technical CA Final subjects. Students who perform well in Financial Reporting and Advanced Financial Management often feel more prepared for professional roles in finance, audit, reporting, and advisory. Clearing Group 1 first also reduces the pressure for the next attempt because students can focus completely on Group 2 taxation and case-study subjects.

CA Final Group 2 Overview

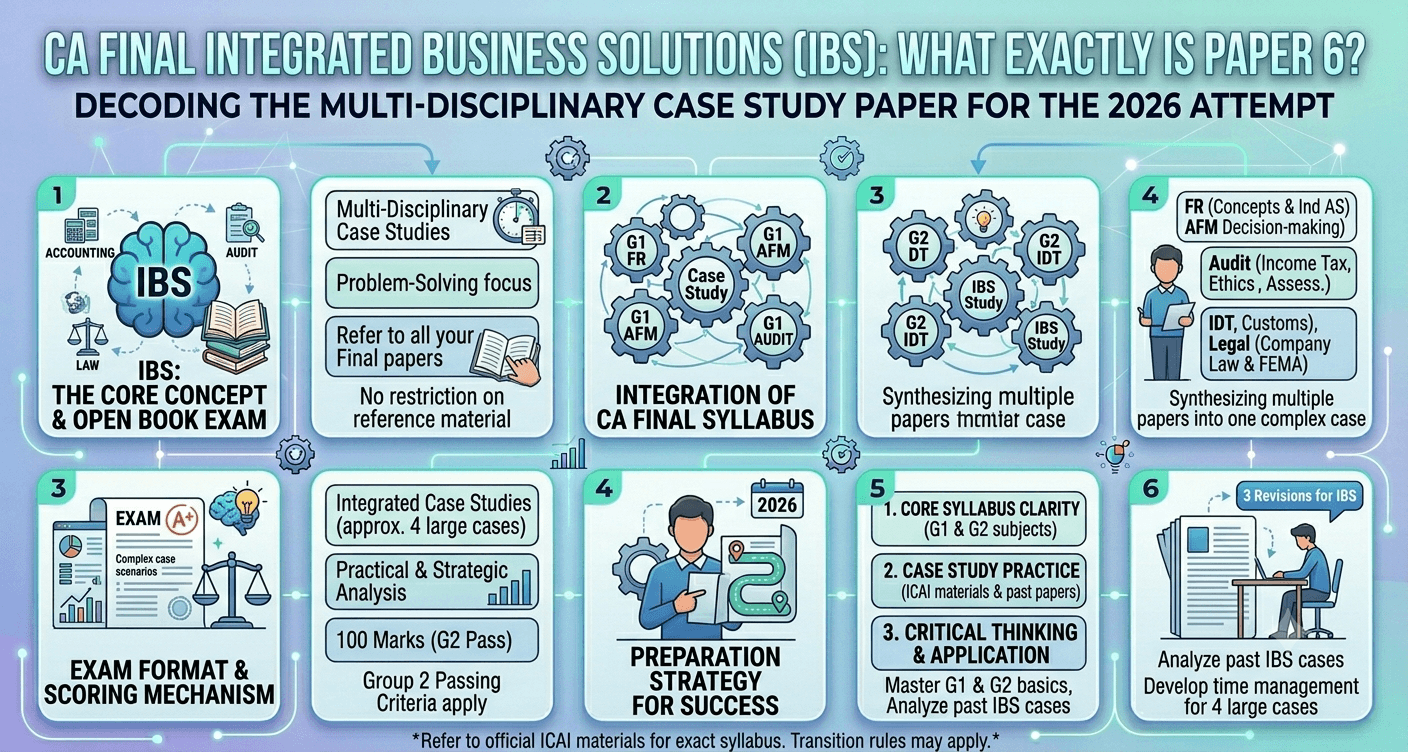

CA Final Group 2 includes Direct Tax Laws & International Taxation, Indirect Tax Laws, and Integrated Business Solutions. This group is suitable for students who are strong in taxation, amendments, GST, customs, legal interpretation, and case-study-based analysis. Group 2 can be scoring when students revise regularly and practise practical questions, but it becomes risky when students forget provisions, miss amendments, or leave case-study practice until the last stage.

Key Risks in Group 2: The major risks in Group 2 are poor retention, missed amendments, incorrect application of tax provisions, and weak case-study handling. Direct Tax and Indirect Tax require repeated revision because they include several rules, limits, exemptions, conditions, and practical treatments. Integrated Business Solutions also requires analytical thinking, so students need to practise case-based questions instead of depending only on theory reading.

Key Rewards in Group 2: The main reward of Group 2 is that taxation papers can offer strong scoring opportunities for students who prepare systematically. Students who revise provisions multiple times and practise exam-style questions can improve accuracy and confidence. Clearing Group 2 first can also be useful for students whose tax preparation is fresh and who want to complete the revision-heavy part of CA Final before moving to Group 1.

CA Final Group 1 vs Group 2: Risk-Reward Analysis

The risk-reward analysis of CA Final Group 1 vs Group 2 depends on the student’s current preparation level. Group 1 has higher technical risk because it includes practical and judgement-based subjects, while Group 2 has higher revision risk because taxation requires regular recall and accurate application. Neither group is automatically easier or more scoring for everyone. The better group is the one where the student has stronger concepts, better revision, and higher mock test confidence.

Student Situation | Better Attempt Choice |

| Strong in accounts, finance, and audit | Group 1 |

| Strong in tax, GST, and case studies | Group 2 |

| Syllabus completed with multiple revisions | Both Groups |

| Limited time or weak revision | Single Group |

| Working or articleship pressure | Stronger prepared group first |

| Repeat attempt with clear weak areas | Focused single group strategy |

Should You Attempt CA Final Group 1 First?

You should attempt CA Final Group 1 first if you are confident in Financial Reporting, Advanced Financial Management, and Auditing. This option is better when your practical concepts are clear, your classes are complete, and you have enough time for question practice and mock tests. Group 1 first can also be useful when your tax preparation is incomplete or when you need more time to revise amendments properly before attempting Group 2.

Should You Attempt CA Final Group 2 First?: You should attempt CA Final Group 2 first if you are stronger in Direct Tax, Indirect Tax, amendments, and Integrated Business Solutions. This strategy works well when your tax preparation is fresh and you can revise provisions multiple times before the exam. Group 2 first is also practical for students who are not yet confident in Financial Reporting or Advanced Financial Management and want to avoid unnecessary technical pressure in the current attempt.

Should You Attempt Both CA Final Groups Together?

Attempting both CA Final groups together can be rewarding, but only when preparation is strong across all six papers. Students should choose both groups if the syllabus is complete, revisions are planned, mock test results are satisfactory, and exam confidence is stable. The benefit is the chance to clear CA Final faster, but the risk is syllabus overload, weak retention, and lack of proper revision. Students should not choose both groups only because others are doing it.

Recommended Study Strategy for CA Final Group 1

For CA Final Group 1, students should focus on concept clarity, daily practical question-solving, audit writing practice, and mock test analysis. Financial Reporting and Advanced Financial Management should be revised through regular problem-solving, while Advanced Auditing should be prepared through standards, keywords, short notes, and structured answer writing. In the last 30 days, students should avoid starting too many new topics and focus on revision, mock tests, mistake correction, and high-weightage areas.

Recommended Study Strategy for CA Final Group 2

For CA Final Group 2, students should focus on repeated tax revision, amendment coverage, practical questions, and case-study practice. Direct Tax and Indirect Tax should be revised multiple times because retention is critical in these subjects. Integrated Business Solutions should be practised through case scenarios to improve reading speed, issue identification, and answer structure. In the final month, students should revise provisions, solve full syllabus tests, and correct mistakes from previous mock papers.

Common Reasons Students Choose the Wrong Group Strategy

Many students fail to perform well because they choose their attempt based on fear, pressure, or overconfidence instead of actual readiness. Common mistakes include attempting both groups without enough revision, ignoring mock test performance, depending only on completed classes, giving too much time to strong subjects, and not analysing previous mistakes. A better strategy should be based on syllabus completion, subject strength, revision quality, test scores, and available study hours.

How CA Test Series Helps Students Prepare Better

CA Test Series helps CA Final students prepare with ICAI-pattern test papers, chapter-wise practice, group-wise test series, full syllabus mock exams, expert answer evaluation, and performance feedback. These tools help students identify weak chapters, improve time management, understand answer presentations, and check whether they are ready for Group 1, Group 2, or both groups. Instead of guessing their preparation level, students can use test performance to make a smarter attempt decision.

Conclusion

The decision between CA Final Group 1 vs Group 2 should be based on preparation level, subject strength, revision status, available time, and mock test performance. Group 1 is suitable for students strong in technical and practical subjects, while Group 2 is suitable for students strong in taxation and case-study-based application. Both groups should be attempted only when preparation is complete and confidence is backed by test performance. With ICAI-pattern mock tests, expert evaluation, and performance analysis from CA Test Series, students can choose the right strategy and prepare with better clarity.