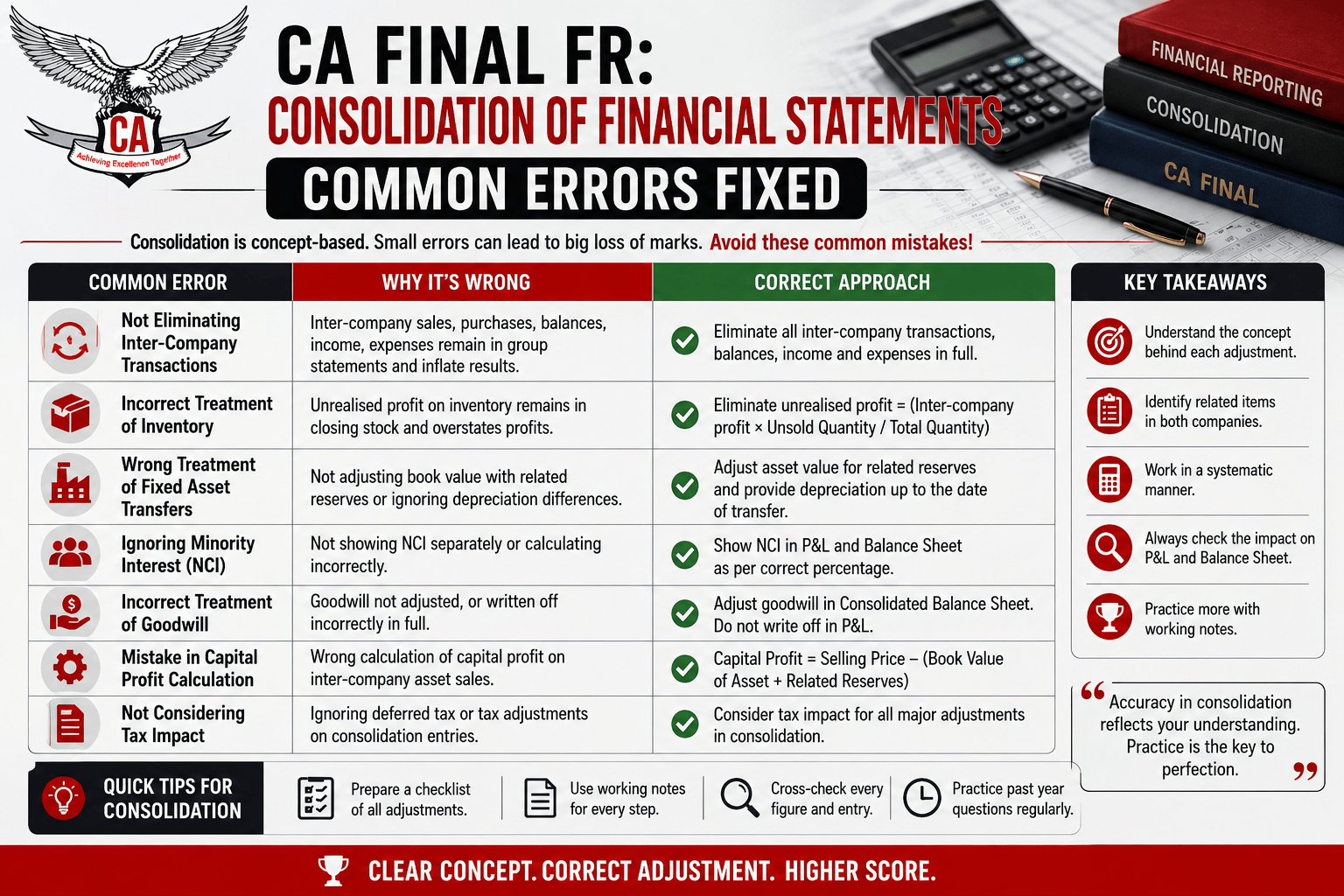

CA Final FR: Consolidation of Financial Statements: Common Errors Fixed

CA Final FR: Consolidation of Financial Statements is one of the most important and challenging areas in Financial Reporting because it tests both accounting logic and exam presentation. Many students understand the basic concept of consolidation but lose marks due to wrong acquisition-date treatment, incorrect goodwill calculation, missed intra-group adjustments, weak working notes, and poor final statement presentation. ICAI’s CA Final Financial Reporting study material includes Chapter 13 on Consolidated and Separate Financial Statements, including Ind AS 110 and consolidation procedures, so students should prepare this topic with proper concept clarity and regular exam-style practice.

What Is Consolidation of Financial Statements in CA Final FR?

Consolidation of Financial Statements means preparing the financial statements of a parent company and its subsidiaries as one combined economic entity. In CA Final FR, students must combine assets, liabilities, equity, income, expenses, and reserves while removing transactions that happened within the group. The purpose is not just to add figures together, but to present the financial position and performance of the group as if it were a single reporting entity.

Meaning of Consolidated Financial Statements: Consolidated Financial Statements show the parent company and its subsidiaries together as one group. The parent controls the subsidiary, so the subsidiary’s assets, liabilities, income, and expenses are included in the group accounts after making necessary adjustments. These adjustments usually include goodwill or capital reserve, non-controlling interest, intra-group transactions, unrealised profit, and pre-acquisition and post-acquisition profit split.

Key Ind AS Standards Related to Consolidation: The most important standard for this topic is Ind AS 110, Consolidated Financial Statements. Students should also understand the link with Ind AS 103 for business combinations, Ind AS 111 for joint arrangements, Ind AS 112 for disclosure of interests in other entities, and Ind AS 28 for associates and joint ventures. ICAI’s educational material on Ind AS 110 explains that the standard deals with the presentation and preparation of consolidated financial statements when an entity controls one or more entities.

CA Final FR Consolidation: Quick Exam Overview

CA Final FR consolidation questions usually test practical application, calculation accuracy, and structured presentation. Questions may include holding-subsidiary relationships, acquisition during the year, fair value adjustments, dividend treatment, inter-company balances, unrealised profit in inventory, asset transfers, goodwill, capital reserve, NCI, and final consolidated balance sheet preparation.

Common Question Patterns in ICAI-Style Papers: Common ICAI-style question patterns include calculation of acquisition-date net assets, pre-acquisition and post-acquisition reserves, goodwill or capital reserve, group reserves, NCI, inter-company sales, debtors and creditors elimination, and unrealised profit adjustment. Students should identify these points while reading the question before starting the final answer.

Core Concepts Students Must Know Before Solving Consolidation Questions

Before solving consolidation problems, students must understand control, date of acquisition, pre-acquisition profit, post-acquisition profit, goodwill, capital reserve, non-controlling interest, intra-group elimination, and unrealised profit. These concepts are connected, so one wrong figure can affect several parts of the final answer.

Holding Company, Subsidiary, and Control: A holding company is a company that controls another company, and the controlled company is called a subsidiary. In consolidation, control is more important than only ownership percentage. Students should check whether the parent has power over the subsidiary and whether it can affect returns through that power. If control is misunderstood, the entire consolidation treatment can become incorrect.

Date of Acquisition: The date of acquisition is the date on which the parent obtains control over the subsidiary. This date is important because it separates pre-acquisition and post-acquisition profits. Pre-acquisition profits are used for goodwill or capital reserve calculation, while post-acquisition profits are shared between the parent and NCI.

Non-Controlling Interest: Non-controlling interest, or NCI, represents the portion of the subsidiary that belongs to shareholders other than the parent. In CA Final FR consolidation, NCI must be calculated carefully because it affects the equity section of the consolidated balance sheet. Students often make mistakes by ignoring NCI’s share in post-acquisition profits, fair value adjustments, or unrealised profit.

Common Errors in CA Final FR Consolidation and How to Fix Them

Students usually make consolidation mistakes because the topic includes many linked adjustments. The best way to fix these errors is to follow a fixed solving sequence, prepare separate working notes, and check whether each adjustment affects goodwill, NCI, group reserves, assets, liabilities, or profit.

Common Error | Why It Happens | Correct Treatment | Exam Tip |

| Wrong acquisition date | Student misses the control date | Split profits from the correct acquisition date | Underline the date first |

| Wrong goodwill calculation | Incorrect net assets are used | Use acquisition-date net assets only | Prepare a separate goodwill note |

| Incorrect NCI | Reserves or profit share is ignored | Include NCI share of relevant net assets | Check ownership percentage twice |

| Missed intra-group balance | Debtors and creditors are not matched | Eliminate internal balances | Compare both company records |

| Missed unrealised profit | Closing inventory is not checked | Remove unrealised profit from inventory | Identify seller and buyer |

| Poor presentation | Working notes are unclear | Use structured notes | Follow ICAI-style format |

Misidentifying the Date of Acquisition: If the acquisition date is wrong, the split between pre-acquisition and post-acquisition profits will also be wrong. To avoid this, students should mark the exact date of control before calculating goodwill, NCI, or group reserves.

Wrong Calculation of Goodwill or Capital Reserve: Goodwill or capital reserve errors happen when students use the wrong net assets, ignore fair value adjustments, or include post-acquisition profits. The correct method is to compare the cost of investment with the parent’s share in the subsidiary’s net assets at the acquisition date.

Incorrect Non-Controlling Interest Calculation: NCI mistakes happen when students calculate only the outside shareholders’ share in capital and ignore reserves, profits, or fair value adjustments. Students should prepare a separate NCI working note and update it for relevant post-acquisition changes.

Missing Unrealised Profit Adjustments:Unrealised profit arises when goods or assets are sold within the group but have not yet been sold to an outside party. This profit should be eliminated because the group has not earned it from an external customer. Students should also check whether the seller is the parent or subsidiary.

Step-by-Step Method to Solve Consolidation Questions in CA Final FR

A fixed method helps students solve consolidation questions with better accuracy. First, read the question carefully and identify the group structure, acquisition date, holding percentage, reserves, and adjustments. Then prepare working notes for net assets, goodwill or capital reserve, NCI, group reserves, intra-group eliminations, and unrealised profit. Finally, prepare the consolidated statement and cross-check every final figure with the working notes.

Important Working Notes Required: The most important working notes are shareholding pattern, net assets, goodwill or capital reserve, NCI, group reserves, unrealised profit, and final consolidated balance sheet figures. Students should not write only the final answer because working notes show the logic behind the calculation and help secure step-wise marks.

CA Final FR Consolidation Adjustments Students Should Not Miss

Students should carefully check inter-company sales and purchases, inter-company debtors and creditors, inventory held from group transactions, depreciable asset transfers, proposed dividend, dividend received, preference shares, bonus shares, right shares, fair value changes, and tax impact. These adjustments may look small, but they can affect several final figures if missed.

Inter-Company Transactions: Inter-company sales, purchases, debtors, creditors, loans, and other internal balances must be eliminated because the group is treated as one entity. If one group company shows receivable and another shows payable, both should be removed from the consolidated balance sheet after checking any mismatch.

Inventory and Asset Transfer Adjustments: If inventory includes profit from an internal group sale, the unrealised profit must be removed. If a depreciable asset is transferred within the group, students should eliminate the unrealised profit and correct the depreciation impact. Many students adjust only one part and lose marks on the second adjustment.

Presentation Tips to Score Better in CA Final FR Consolidation

A good presentation is important because consolidation answers are lengthy. Students should use clear working notes, proper headings, neat columns, logical calculation order, and final figures that match the working notes. Avoid overwriting, unclear figures, and mixed calculations. A clean answer helps the evaluator follow the solution easily.

How to Practice Consolidation for CA Final FR

Students should start with basic holding-subsidiary questions, then move to advanced adjustment-based problems, and finally solve full-length consolidation questions. Practice should include ICAI study material, revision questions, chapter-wise tests, and full-syllabus mock tests. After every test, students should review whether mistakes were conceptual, calculation-based, presentation-related, or due to time pressure.

How CA Test Series Helps Fix CA Final FR Consolidation Errors

CA Test Series helps students improve consolidation preparation through ICAI-pattern FR test papers, chapter-wise consolidation practice, full-syllabus CA Final FR mock tests, expert evaluation, mistake analysis, and performance feedback. This helps students identify weak areas such as goodwill, NCI, group reserves, unrealised profit, and working note presentation before the final exam.

CA Final FR Consolidation Preparation Checklist

Checklist Area | What to Review | Status |

| Concept clarity | Control, acquisition date, NCI, goodwill, group reserves | Pending / Done |

| Formats | Goodwill, NCI, net assets, consolidated balance sheet | Pending / Done |

| Adjustments | Intra-group sales, inventory profit, dividends, asset transfers | Pending / Done |

| Working notes | Shareholding, net assets, goodwill, NCI, group reserves | Pending / Done |

| Mock tests | Time management, accuracy, presentation, missed adjustments | Pending / Done |

| Final revision | Mistake notebook, difficult adjustments, key solved questions | Pending / Done |

Common Revision Mistakes Students Should Avoid

Students should avoid memorising formats without understanding logic, skipping difficult adjustments, practicing only short questions, ignoring past mistakes, and revising consolidation only through reading. CA Final FR consolidation needs written practice because students often understand the answer while reading but struggle when solving independently under exam pressure..

Conclusion

CA Final FR: Consolidation of Financial Statements is a scoring topic when students prepare it with the right method. Most errors happen due to weak concept clarity, missed adjustments, poor working notes, or lack of timed practice. By understanding Ind AS logic, following a step-by-step solving method, practicing ICAI-pattern questions, and reviewing mistakes regularly, students can improve their performance. CA Test Series supports this preparation with chapter-wise tests, full-syllabus mock exams, expert evaluation, and feedback that helps students fix common consolidation errors before the final exam.