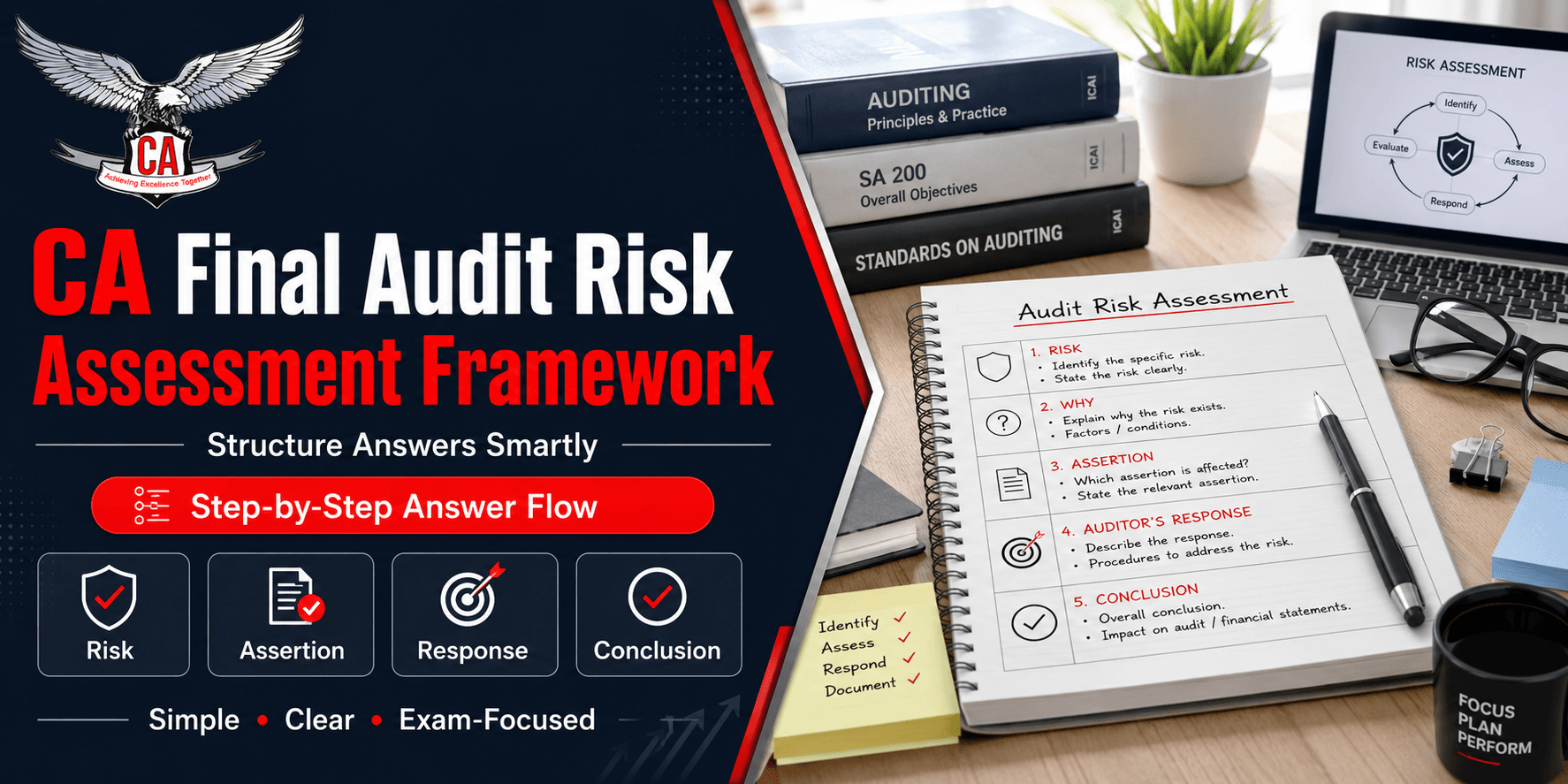

CA Final Audit Risk Assessment Framework: How to Structure Answers

The CA Final Audit Risk Assessment Framework is one of the most useful tools for writing clear, practical, and exam-oriented Audit answers. Many students know the theory of risk assessment, but they lose marks because their answers are too generic, not linked with the case facts, or missing the auditor’s response. A good answer should not simply explain what risk assessment means. It should identify the risk, connect it with the relevant Standard on Auditing, link it with the affected assertion, and explain what the auditor should do next. This guide is based on your draft content and optimized for a CA Final student audience. ICAI lists SA 315 under “Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and Its Environment” and SA 330 under “The Auditor’s Responses to Assessed Risks,” which makes both standards important for this topic.

What Is the CA Final Audit Risk Assessment Framework?

The CA Final Audit Risk Assessment Framework is a structured way of identifying and responding to risks of material misstatement in financial statements. In simple terms, it helps the auditor understand what can go wrong, why it can go wrong, which financial statement area may be affected, and what audit procedures should be performed. For CA Final Audit students, this framework is especially important because it helps convert technical knowledge into a well-structured exam answer.

Meaning of Risk Assessment in Audit

Risk assessment in audit means the process of identifying areas where the financial statements may be materially misstated due to fraud, error, weak internal controls, unusual transactions, estimates, or business complexity. In exam answers, students should explain this meaning briefly and then apply it directly to the case facts.

Objective of Risk Assessment in CA Final Audit

The objective of risk assessment is to help the auditor understand the entity, identify possible risks, assess their impact, and plan suitable audit procedures. In CA Final Audit, students should show that risk assessment is not only about finding risks but also about deciding how the auditor should respond to those risks.

SA 315 and SA 330: How They Fit into Risk Assessment

SA 315 is used when the auditor identifies and assesses risks of material misstatement through understanding the entity and its environment. SA 330 is used after the risks are assessed because it deals with the auditor’s responses to those risks. In exam answers, students can use SA 315 for risk identification and SA 330 for audit procedures, tests of controls, substantive procedures, and overall audit response.

Standard | Main Use in Answer | When to Mention |

| SA 315 | Identifying and assessing risk | When the question involves understanding the entity, internal control, fraud risk, significant risk, or assertion-level risk |

| SA 330 | Auditor’s response to assessed risk | When the question asks what audit procedures or responses should be performed |

| SA 230 | Audit documentation | When the answer requires documentation of risk assessment and audit procedures |

Why the CA Final Audit Risk Assessment Framework Matters in Exams

The CA Final Audit Risk Assessment Framework matters because it helps students write answers that are structured, practical, and examiner-friendly. Audit is not a subject where long theory alone guarantees marks. The examiner expects students to apply audit concepts to the given situation. A structured framework helps students present the issue, identify the risk, explain the reason, link the assertion, and write the auditor’s response in a logical order.

Key Benefits for Students

This framework improves case-based answer writing because it prevents random and scattered points. It also helps students connect Standards on Auditing with practical audit procedures. Most importantly, it makes the answer easier to read, because the examiner can quickly see the risk identified, the reason behind it, the affected assertion, and the audit response.

Key Components of the CA Final Audit Risk Assessment Framework

A strong risk assessment answer usually includes understanding the entity, understanding internal control, identifying the risk of material misstatement, assessing risk at the financial statement or assertion level, identifying significant risks, and designing the auditor’s response. These components work like a checklist for writing complete Audit answers.

Component | What It Means | Exam Writing Use |

| Understanding the entity | Knowledge of business, industry, regulations, accounting policies, and operations | Helps explain why the risk exists |

| Internal control | System used to prevent or detect errors and fraud | Helps identify control risk |

| Risk of material misstatement | Possibility that financial statements may be materially wrong | Forms the main point of the answer |

| Assertion-level risk | Risk affecting a specific balance, transaction, or disclosure | Helps connect risk with audit procedures |

| Significant risk | Risk requiring special audit consideration | Useful in fraud, estimates, revenue, and related party cases |

| Auditor’s response | Procedures performed to address the risk | Completes the answer |

Step-by-Step Framework to Structure Risk Assessment Answers

Students should follow a simple step-by-step structure while writing risk assessment answers. First, read the requirement carefully. Second, identify the relevant audit standard. Third, extract risk indicators from the case. Fourth, classify the risk properly. Fifth, link the risk with the relevant assertion. Sixth, write the auditor’s response. Finally, conclude with professional judgement.

Practical Answer Flow

Step | What to Do | Example Writing Approach |

| 1 | Read the requirement | Identify whether the question asks for risk, comment, procedure, or responsibility |

| 2 | Mention relevant SA | Use SA 315 for risk assessment and SA 330 for response |

| 3 | Pick case facts | Identify weak controls, unusual entries, estimates, or pressure on management |

| 4 | State the risk | Write the exact risk, such as overstatement of revenue |

| 5 | Link assertion | Connect with completeness, existence, accuracy, valuation, or disclosure |

| 6 | Write response | Mention suitable audit procedures |

| 7 | Conclude | Give a short professional conclusion |

Best Answer Format for CA Final Audit Risk Assessment Questions

The best answer format is: relevant standard, case fact, risk identified, assertion affected, auditor’s response, and conclusion. This format keeps the answer short, complete, and easy for the examiner to evaluate. Students should avoid writing vague lines such as “there is audit risk” and instead mention the exact financial statement risk.

Sample Answer Format

As per SA 315, the auditor is required to identify and assess risks of material misstatement through understanding the entity and its environment. In the given case, the presence of weak approval controls may create a risk of unauthorized transactions. This may affect the accuracy and completeness assertions. The auditor should test relevant controls, inspect supporting documents, verify approvals, and perform substantive procedures to obtain sufficient appropriate audit evidence.

How to Connect Risk Assessment with Assertions

Assertions help students explain exactly where the financial statement may be misstated. For example, fake sales may affect existence, unrecorded expenses may affect completeness, wrong calculations may affect accuracy, obsolete inventory may affect valuation, and related party transactions may affect presentation and disclosure.

Assertion | Meaning | Common Risk Example |

| Completeness | All required transactions are recorded | Unrecorded liabilities or missing expenses |

| Accuracy | Amounts are recorded correctly | Wrong invoice value or calculation error |

| Existence | Recorded items actually exist | Fake sales or non-existent debtors |

| Valuation | Items are recorded at proper value | Obsolete inventory or doubtful debts |

| Rights and obligations | Entity has legal rights or obligations | Pledged assets or disputed liabilities |

| Presentation and disclosure | Items are properly classified and disclosed | Related party or contingent liability disclosure |

How to Write Auditor’s Response After Risk Assessment

After identifying the risk, students must write the auditor’s response. This may include overall responses, further audit procedures, tests of controls, substantive procedures, and documentation. The response should match the case facts. For example, if the risk relates to receivables, the auditor may obtain external confirmations. If the risk relates to inventory valuation, the auditor may check ageing, net realizable value, and subsequent sales.

Common Mistakes in CA Final Audit Risk Assessment Answers

Many students lose marks because they write generic theory without applying it to the case. Other common mistakes include not mentioning the relevant SA, ignoring assertions, writing only the risk without the auditor’s response, using long paragraphs, and missing the conclusion. A good answer should be specific, standard-based, case-linked, and professionally presented.

Presentation Tips for Scoring Better

Use headings and subheadings such as “Relevant Standard,” “Risk Identified,” “Assertion Affected,” “Auditor’s Response,” and “Conclusion.” Write in points instead of long paragraphs. Use standard-based language like “risk of material misstatement,” “sufficient appropriate audit evidence,” “assertion level,” and “substantive procedures.” Keep the answer case-specific and avoid overwriting.

How CA Test Series Helps You Improve Audit Answer Writing

CA Test Series helps CA Final students improve their Audit preparation through ICAI-pattern test papers, chapter-wise practice, full syllabus mock exams, expert answer evaluation, and performance feedback. For topics like risk assessment and internal control, regular mock test practice helps students identify weak areas, improve presentation, and learn how to write structured answers under exam conditions.

Quick Revision Table: CA Final Audit Risk Assessment Framework

Area | What to Write in Exam | Examiner Expectation |

| Risk identification | State the exact risk from the case | Clear application, not generic theory |

| Relevant standard | Mention SA 315 or SA 330 where applicable | Correct standard reference |

| Assertion | Link risk with assertion | Shows audit depth |

| Auditor’s response | Write suitable audit procedures | Practical and case-specific answer |

| Conclusion | Close with professional judgement | Complete answer structure |

risk, understanding the entity, internal control, significant risk, or assertion-level risk.

Conclusion

The CA Final Audit Risk Assessment Framework helps students write better Audit answers by connecting standards, case facts, risks, assertions, and audit procedures in a logical manner. Instead of writing long theoretical answers, students should focus on structured presentation and practical application. With regular mock test practice and expert evaluation from CA Test Series, students can improve their Audit answer writing and perform better in CA Final exams.